You are attempting to access a website operated by an entity not regulated in the EU. Products and services on this website do not comply with EU laws or ESMA investor-protection standards.

As an EU resident, you cannot proceed to the offshore website.

Please continue on the EU-regulated website to ensure full regulatory protection.

화요일 Jul 9 2024 10:56

6 분

The FTSE 100 struggled to make much headway early doors with BP shares down 3.5% on a $2 billion impairment and weak refining margins. I guess investors should be cheered up by the fact Saudi Aramco is making a big bet on internal combustion engines being around for a “very, very long time”.

Shares in BP are down almost 3% year-to-date despite a close to 10% rally for Brent crude. Trying to do all the green stuff, meet carbon targets and run a complex, profitable energy business is not so easy.

But the blue chips did manage to open a bit higher above 8,200 and London looks stronger than the rest of Europe, with Paris and Frankfurt nursing losses of around half a percent. Yesterday was all pretty flat in the wake of the French election result, which offered no more clarity than before. Societe Generale shares are down 1%.

Franco-German bond spreads (see chart below) are still elevated — the sense is that there are not really any good outcomes from this result for governing France, for Macron’s pro-business agenda or his personal standing, for sorting the fiscal mess.

You can imagine the situation being untenable soon, forcing Macron to call a presidential election. The UK looks like an island of calm and political stability in comparison!

Across the pond, Joe Biden told Democrats that he’s “in it to the end”, which has a relatively ominous ring to it. Fed Chair Powell was also headed to Capitol Hill to deliver his twice-yearly report on the state of the economy, with investors closely watching for cues of interest rate cuts.

As for Biden, as we discuss in this week’s upcoming edition of the Overleveraged podcast, there are not really any good alternatives for the Democrats – if he can’t run now, how can he be commander-in-chief for 6 more months?

The Labour government set about its economic duties swiftly with some announcements yesterday focused on housebuilding. Sterling tested a month high but has come back a bit overnight to rest at $1.28.

Federal Reserve Chair Jay Powell is due to testify on monetary policy in front of the Senate Banking Committee today. Last week in Sintra he indicated the Fed is not in a rush to cut rates:

“We want to be more confident that inflation is moving sustainably down toward 2% before we start the process of … loosening policy.”

But staying put on interest rates means tightening, since real rates are on the rise. We are seeing bear steepening in the Treasury curve – the view is that Donald Trump back in the White House is going to pile on more debt, cut taxes and drive growth, which ought to be good for stocks and bad for bonds. Markets seem to be, tentatively at least, positioning for a more inflationary environment than we have now. Which might explain why the Fed is playing for time. June’s CPI inflation report is due on Thursday and follows signs of a cooling US labour market.

If investors are seeing a Trump win, then clearly, they think it’s good for stocks. The S&P 500 and Nasdaq again closed at record highs on Monday. But concentration and breadth are not strong – the five largest stocks in the S&P 500 now account for 29% of the index. Meanwhile the Nikkei 225 hit a fresh record high, led by tech and chipmakers.

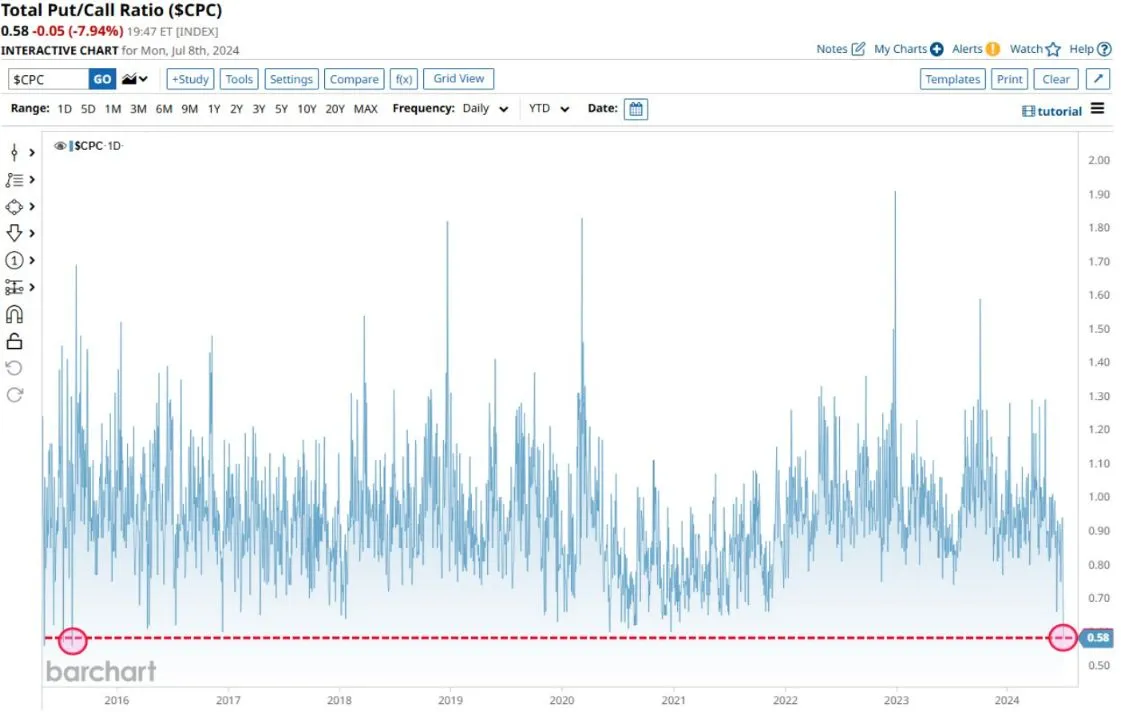

Put-call ratio at 0.58, lowest since Aug 2015.

Looking ahead to the overnight session later, the Reserve Bank of New Zealand (RBNZ) will likely leave its official cash rate (OCR) on hold at 5.5% and emphasize the upside risks to inflation. The central bank was unexpectedly hawkish at its last meeting in May, revising up its forward OCR profile. This new outlook suggested an increased chance of a further rate hike (perhaps in November) and a delay to eventual cuts to August next year.

Crude oil extended its decline off Friday’s more than two-month high to hit its lowest in a week. Watching the MACD crossover.

위험 고지: 본 기사는 저자의 견해만을 반영하며, 정보 제공 목적으로만 작성되었습니다. 이는 투자 조언, 투자 리서치 또는 거래 권유를 구성하지 않으며, Markets.com 플랫폼의 입장을 대변하지도 않습니다. 주식, 지수, 외환(FX), 원자재의 거래 및 가격 예측을 고려할 때, CFD 거래에는 상당한 수준의 위험이 수반되며 모든 투자자에게 적합하지 않을 수 있음을 유의하시기 바랍니다. 레버리지 상품은 원금 손실을 초래할 수 있습니다. 과거의 성과는 미래의 결과를 보장하지 않습니다. 거래 전에 관련된 위험을 완전히 이해하고, 투자 목표와 경험 수준을 고려하십시오. 암호화폐 CFD 및 스프레드 베팅 거래는 모든 영국 소매 고객에게 제한됩니다.

최신

모두 보기토요일, 25 10월 2025

3 분

금요일, 24 10월 2025

4 분

금요일, 24 10월 2025

3 분